PART III: Debt Reform in Finland- Fixing a Broken System

This is not just my story — it’s a broken system. In Part III, I lay out why Finland’s debt adjustment laws must change, and how reform could finally bring fairness.

Miia Hiltunen

9/5/20258 min read

WHY DEBT REFORM IN FINLAND MATTERS TO EVERYONE

Those dark, cold Finnish winter days — I would lie in bed, hopeless, unable to move. I knew that if I got up and went swimming, I might feel better, but I was incapable of moving even an inch. All I could do was pull the covers over my head and sink into a deep sleep. Outside, the snow lay untouched, silent and still. Inside, my body was exhausted, but my thoughts refused to rest. That’s when the darkest questions crept in: maybe everyone would be better off if I wasn’t here.

I can tell you I’ve had my share of those nights — the kind where there’s no light at the end of the tunnel, only the suffocating weight of hopelessness pressing down.

These past few years have been the closest I have ever gotten to thinking about suicide and understanding those who have actually gone through with it.

The emptiness a person feels, thinking there is no way out. That’s severe depression for you.

Sounds familiar.

At the same time, for many who haven’t experienced depressive episodes, feeling so miserable, feeling the walls closing in on you, may seem incomprehensible, as if things couldn’t be that bad.

Around 94% of the Finnish population actually doesn’t know how it truly feels to be depressed.

But depression is real, and many who commit suicide were depressed.

It’s unimaginable that people suffering from financial problems — like me when I was in debt adjustment — are made to feel this way by the very government that was once a trailblazer in suicide prevention back in the 1990s.

To show so little regard for its citizens, the very building blocks of the economy, is beyond comprehension.

Whether or not that’s the intention, the effect is the same: the Justice Department’s system pushes people into setbacks so deep that it takes years to recover — if they ever truly do — and the toll is mental as much as physical. This all has to do with the structure of the debt adjustment plan and how a debtor is forced to live for 3-5 years, more on that in Part I of this series.

Maybe you are thinking, she’s overplaying it, but am I?

A 2025 Norwegian study by Carla Hughes and Åsmund Hermansen for the Scandinavian Journal of Public Health titled "Payment Problems and Suicide: Life Under Financial Strain," the authors studied the impact of payment problems on suicide.

From their longitudinal study, they found that those facing payment problems within the Norwegian population between 2009 and 2018 were at higher risk of suicide, this is both men and women. Furthermore, when adjusting for demographic variables, they found that women who were experiencing financial hardship were even more susceptible to suicide in comparison to their male counterparts. The study suggests more protection is required for those coping with financial issues and highlights an important area for improvement within gender-sensitive health and social interventions.

The same can be applied to Finland. Many international studies have shown that financial woes, in addition to depression and anxiety disorders, lead to self-harm.

There is also a connection between those who have suffered traumatic and stressful events to suicide.

Annually, more than 700,000 people die by suicide, and the World Health Organisation has characterised suicide as a serious 'universal public health issue..

And so it should be. In Finland, 752 people committed suicide in 2023.

No one should be made to feel that their only way out is by ending their life.

Entrepreneurship itself is HARD and should a person have given it their all and not succeeded, they should not be made to feel like they are a failure by the government and society.

Policy makers need a wake-up call to the reality of real life in Finland.

THE FLAWS IN FINLAND'S DEBT ADJUSTMENT SYSTEM

It's easy for policymakers to sit in their nice plush office and put numbers to paper when the system they use is flawed.

In debt adjustment, creating a family budget with outdated grocery prices, assuming perfect health, and ignoring today’s real living costs simply doesn’t work.

As I mentioned in my last post,

“Sufficient monthly funds must be reserved for the debtor’s livelihood during the program, and it should not lead to a need for social assistance or to further indebtedness.”

But if we look at the facts, it’s not only me who says debt adjustment is unmanageable. In 2019 alone, over 4600 repayment plans had to be enforced through debt collections because people could not keep up with the strict schedules.

Clearly, something is NOT adding up. Or the numbers might add up on their spreadsheet models, but they crumble upon contact with the harsh reality of inflation and the complex needs of real households.

HOW STRICT BANKRUPTCY LAWS HURT FINLAND'S ECONOMY

Wouldn’t it be wise to do everything in your power to get these people back on their feet and into the workforce?

How is it that Finland doesn’t want these types of people in their economy?

Entrepreneurs are notoriously hard-working, committed, and motivated.

Why not give them a real chance to start new businesses and create jobs — bringing fresh tax income, growth, and much-needed renewal to Finland’s struggling economy?

Finland's economy never recovered from the global financial crisis. During the good ole days of Nokia, between 2000 and 2008 Finland's productivity grew by a total of 14.6%, but since the global financial crisis labour productivity has only grown a total of 1.1% from 2009-2023. Also since the crisis Finland's GDP per capita has not grown.

The Bank of Finland itself is calling for new investment, new skills and new growth.

My ultimate goal was also to contribute to that. Yet when my business failed, Finland's insolvency legislation, specifically the Debt Adjustment Act didn't see an entrepreneur who needs support to try again. Instead, it treats people in a way that punishes risk-taking and discourages the very entrepreneurial activity this country needs the most.

This has been my mantra for years now; for Finland's economy to grow, entrepreneurship should be supported (as should failed entrepreneurs), nurtured, and not frowned upon. The debt adjustment robs a person of their dignity and puts their life on hold for 3-5 years, all while they could be contributing to the economy.

For example, second-time founders, when given the opportunity, have an average success rate of 30 percent. Compare that to first-time founders who have an 18% rate of success.

What am I, and thousands of others like me in this equation? We are the very human capital the Bank of Finland says the country desperately needs to secure its future. By punishing failure instead of fostering a second chance, the current Debt Adjustment Act is actively destroying the exact resource it should be trying to rebuild.

This takes me to a topic dear to my heart, the culture of failure, which is prevalent in Finnish society, and will be addressed in my next blog post.

Not only does it discourage entrepreneurship, but when someone fails, they will FEEL IT from all around.

THE ROAD TO BANKRUPTCY REFORM IN FINLAND

First Finland must address their negative attitude towards failure, as it reflects how entrepreneurship and bankruptcy are perceived.

I call for a “Yes to Entrepreneurship” Project (working title) sponsored by the Ministry of Economic Affairs and Employment in collaboration with the Ministry of Education & Culture, Finnish Entrepreneurs ( Suomen Yrittäjät), Business Finland, universities, Mieli Ry, and international partners ( Nordic Innovation, EU Commision).

The mission of the project is to,

"To reshape Finland’s cultural and societal attitudes toward entrepreneurship, failure, and resilience by reducing the stigma of bankruptcy and normalizing entrepreneurial risk-taking as part of a healthy economy."

The project’s goals would be split into four categories:

1. Cultural Reframing of Failure

2. Reducing Stigma around Bankruptcy

3. Encouraging Healthy Individualism

4. Boosting Entrepreneurial Participation

Together, these goals form the foundation for cultural and legislative change — because awareness without reform is only half the solution.

These aren’t abstract ideals; they’re exactly the shifts Finland needs if we want to move beyond survival and toward renewal. Without reframing failure, reducing stigma, and making space for healthier individualism, entrepreneurial participation will remain weak—and so will our economy.

That’s why, from the very beginning, I knew this blog series had to end with reform. Shaping people’s perspectives is the first battle, but changing the law is the harder one—and both are necessary. I’m not yet in a position to draft the exact legal amendments, because that takes careful, line-by-line work.

Still, one thing is clear: Finland’s bankruptcy and debt adjustment laws are outdated, and they need reform. My role right now is to make that urgency impossible to ignore.

One thing for sure, failure in business is not an anomaly — it’s built into how market economies work.

In fact, it’s one of their defining features. As Joseph Schumpeter, one of the most renown economists of the 20th century, argued in his theory of creative destruction , business failures are not only normal but necessary, driving entrepreneurship and innovation forward.

A 2020 study by Sylwia Morawska, Błażej Prusak, Przemysław Banasik , Katarzyna Pustułka, and Bartosz Groele found that many entrepreneurs who go bankrupt return with valuable experience, start again, and often succeed the second time.

Failure can be a powerful form of learning. The real problem arises when failed entrepreneurs are stigmatized — because stigma doesn’t just wound reputations, it actively discourages them from trying again and building new businesses.

There’s always this question: should bankruptcy laws punish people who tried and failed, or should they actually help the honest ones get back on their feet? The truth is, the way the law is written — and how fast or slow the courts handle cases — sets the tone for entrepreneurship and innovation in a country.

Take the U.S. for example. Their system is known as one of the best for business. Failure there isn’t this life-ruining scar like it is in Europe. The laws are built around a second chance. You go under, you regroup, and you’re allowed to start again pretty quickly. Because of that, people aren’t paralyzed by the fear of failure — they take risks, they try new ideas.

And that’s where real innovation comes from. When failure isn’t a dead end, it becomes part of the process. You fall, you learn, you get sharper. A bankruptcy isn’t the end of your story, it’s just one messy chapter before the next.

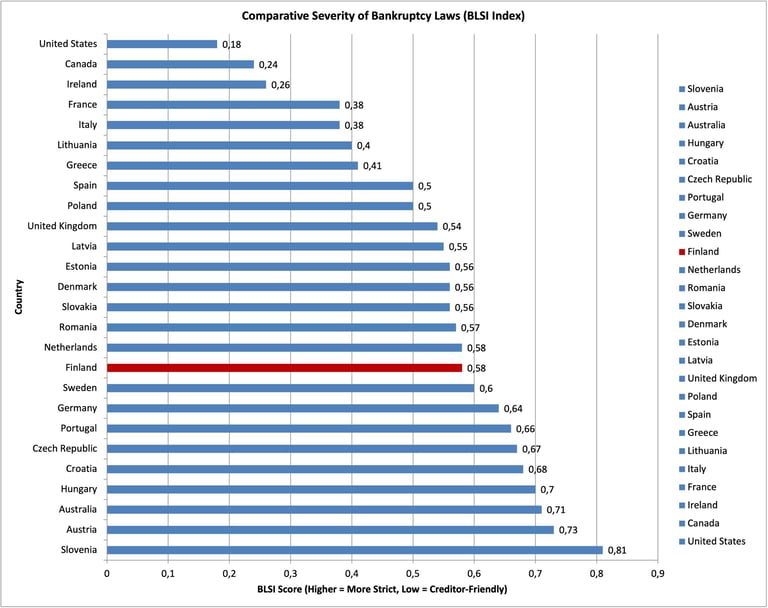

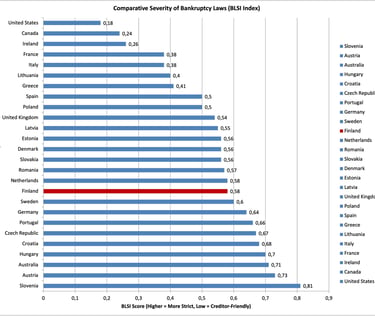

Take the study where researchers compared bankruptcy laws in 27 countries. They built the Bankruptcy Law Severity Index (BLSI) to show which systems punish debtors most harshly and which actually give them a chance to rebuild.

On that scale, Finland sits at 0.58, on the strict end of the scale.

This chart tells the story better than words. Finland is on the wrong side of the divide.

Our law doesn’t just punish failure — it strangles the very entrepreneurial energy the Bank of Finland says we need to survive the next decade.

My suggestions are:

Stop wiping out credit records. Failed entrepreneurs should not lose their credit record.

Base repayment on real living costs — food, energy, housing, children — not outdated numbers.

Automate adjustments with inflation instead of forcing endless amended payment plans.

Fix corporate restructuring so viable businesses actually survive instead of just postponing failure.

End discrimination by Finnvera, the Tax Authority, and grant providers against previously failed entrepreneurs.

CONCLUSION: BUILDING A FAIRER BANKRUPTCY SYSTEM

Failure in business is not a personal flaw. It’s part of how markets work.

Especially today, so many factors that affect businesses — tariffs, interest rates, energy prices, and many others — are things we here in Finland can simply not influence.

But Finland’s laws still treat failure as a permanent scar instead of a step toward growth. The Bankruptcy Law Severity Index proves it: Finland sits on the harsher side, far from debtor‑friendly countries like the U.S., Canada, and Ireland where second chances are real and innovation thrives.

The reforms I’ve laid out are not radical — they’re the bare minimum. Stop wiping out credit records. Base repayment on real living costs. Introduce automatic adjustments instead of forcing people into endless amended plans. Fix corporate restrucutirng so it actually saves viable businesses instead of just postponing death.

Finland must decide: do we keep punishing people for trying, or do we finally create a system that helps people and companies rise again? If we are serious about resilience, innovation, and courage, then the time for reform is now.

Failure is not the end of the story — it’s the beginning of a new one.