Debt Adjustment: One Form of Financial Hell

My three year debt adjustment ended on the 31 of July. I can finally breathe.

8/6/202514 min read

It's FINALLY over.

Looking back to 2021 when I started the process of applying to the debt adjustment, I thought this time would never come. It seemed eons away. But here we are: August 2025 and it's really over. I could pinch myself.

Anybody who has been through this hell knows what I mean. How people have made it through this with their sanity intact I do not know -because I lose mine somewhere along the way.The financial struggle, constant pressure, the toll on your health and peace of mind... it's relentless.

Everyone knows severe financial hardship is real. People commit suicide ovaer it.

It took everything from me. At times I felt like I had a mental block wrapped around my entire life. I couldn'r create. I couldn't think.

What started as a serious content project in February 2023, never went anywhere. Not because I was lazy or lacked time, but because of the emotional strain it put on my psyche.

Every day was excruciating. There were good moments, but they were rare. For most of the past three years, I've been stuck in a cycle of anxiety, long stretches of depression, and anger.

It took the program ending for me to finally feel free. It's like a massive weight has been lifted off my shoulders.

And that's why I am writing this.

This blog is about the emotional and physical toll of debt adjustment due to the immense financial strain it puts on the person who is in the program. And that toll is the "why" behind this blog.

I want to see legal changes to the system- changes that take into account what this program does to people's lives, not just their bank accounts.

FINANCIAL HELL: A SYSTEM STUCK IN THE PAST

It all starts with a great financial burden bestowed upon you when your debt adjustment program commences.

Let's start with the basics, which are defined in the payment plan as the debtor's "essential living expenses." The official term in Finnish is "välttämättömät elinkustannukset." These are defined in the Ministry of Justice Decree on the amendment of sections 4 and 6a of the Ministry of Justice Decree on the grounds for assessing a debtor's ability to pay in private debt adjustment (1034/2021).

Section 4 covers "other essential living expenses" for the debtor and their family, which are food, clothing, ordinary healthcare expenses, personal and home cleanliness, home maintenance, local public transport not relating to commuting, newspaper publications, phone use, hobby and recreational activities, as well as other similar expenses.

They are calculated as such per month:

A debtor living alone, or a debtor who is a single parent, 552 euros.

A debtor living in a marriage or cohabitation, or a debtor living in a joint household with another adult, 465 euros.

The two oldest children under 17 living in the same household with the debtor, 355 euros each, the third oldest and the younger children 331 euros each.

A child aged 17 years or older living in the same household with the debtor, 392 euros.

In my situation, living with my partner and two children (50% of the time) at the time when this program was made, we were allocated €930 per month for basic living expenses, of which I covered €465 per month. But how does the Ministry of Justice get to this figure off which a family of four should live off a month.

It starts with Statistics Finland, which publishes the Cost-of-living Index, which is based on the prices of a set basket of goods and services. Then, Kela, the Social Insurance Institution of Finland, takes the cost-of-living index data and produces the National Pensions Index. This index is meant to keep certain benefits in line with general price level changes. The problem here is that it is not an average across all goods and services, and not a tailored measure for debtors' real expenses. Thus, like what happened in 2021 with the start of the war in Ukraine, when food and electricity prices spiked drastically, the average does not take into account the reality of it all.

Lastly, we get to my debt adjustment calculation. Here, the Ministry of Justice uses Kela's cost-of-living index, and wait for it, they always use the previous year's index in their calculations, further offsetting the true cost of living. In addition to this €465 allowance I had every month, which was meant to cover all living expenses, €260,12 was allocated for my children. Note this is only one period between 1.08.2023-31.07.2024; there were six different types of calculations based on different periods, due to different circumstances.

Then let's take this norm standard of living under the debt adjustment and compare it to a report by Anna-Riitta Lehtinen, for the Centre for Consumer Research located within the University of Helsinki Faculty of Social Sciences, at the University of Helsinki, we will see drastic differences. The report titled "What Does It Cost to Live? Price Update of the Reference Budgets for a Reasonable Minimum for 2021," states at the start that these reference budgets are based on a,

"reasonable minimum level of consumption, which is lower than average consumption but slightly above the low-income threshold."

Lehtinen goes on to discuss how these reference budgets are still at an early drafting stage and that they are still an evolving process, bringing up whether reference budgets should be created for households or individuals. Another important factor mentioned is the need for more households, so as to better understand the needs of different household compositions, life situations, and children at different ages. Then mentioned the need for alternative calculations for goods and their prices, such as those on different diets and housing costs.

The image below shows the cost of living for a family with two children for 2021, figures taken from the report.

Take a 2021 publication from the Department of Justice titled, "Amending Debt Adjustment: A Fresh Start for Entrepreneurs and Improving Debtors' Position." The report goes on to say, that a decent monthly amount should be set aside for the debtor's livelihood during the duration of the program, and that it should not lead to a need for social assistance or further indebtedness.

Funnily enough, when in debt adjustment, one is not meant to accur any new debt, so this whole program is a joke in a sense as to how far it is from reality, and this will be explained next.

"Despite the annual index increase, the cost-of-living standards in debt adjustment are no longer at the originally intended level — that is, one quarter higher than the basic social assistance norms. Unlike the norms for social assistance, the cost-of-living standard in debt adjustment has not been raised in real terms during its existence. As a result, the two standards have gradually converged over time. In some cases, the debt adjustment standard may even become lower than the social assistance norm."

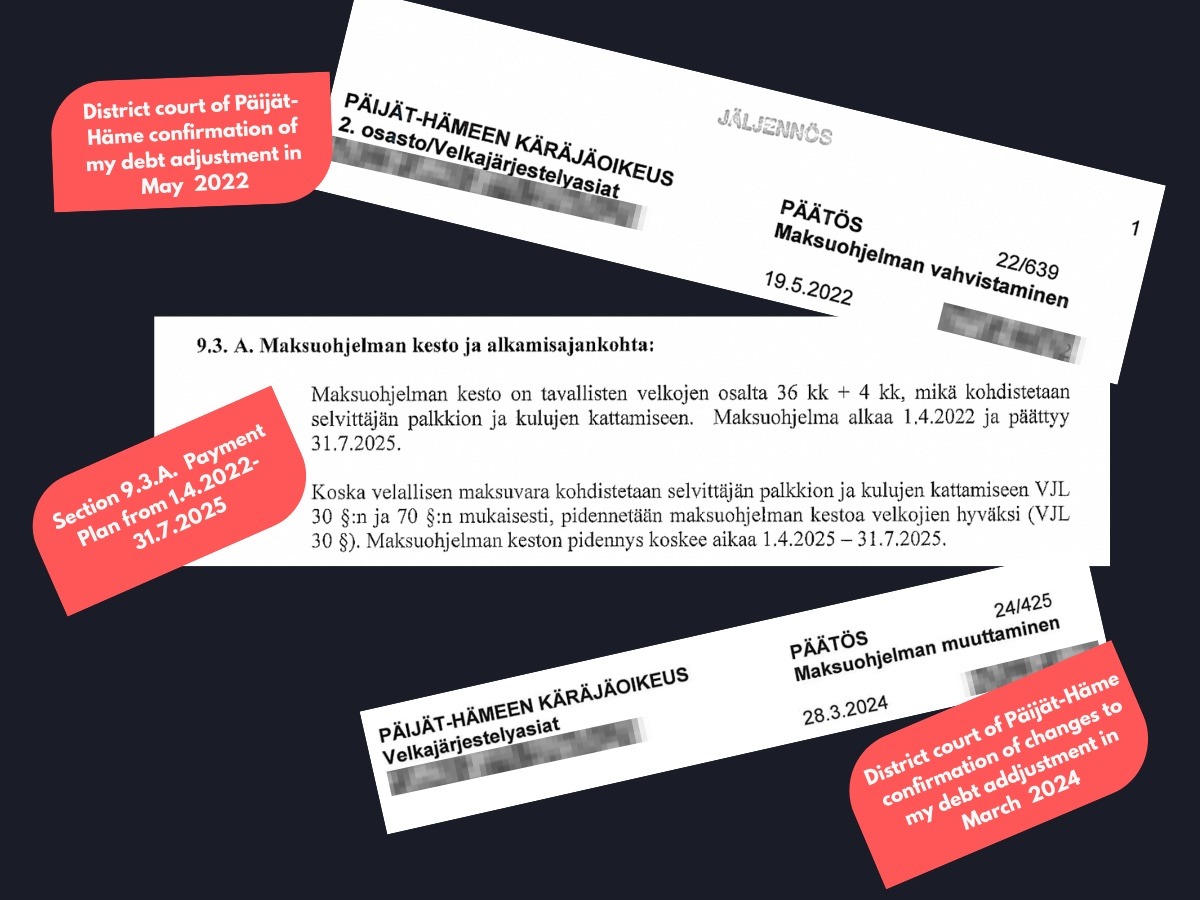

I want to go back to my experience during my debt adjustment. My program was approved by the municipal court in spring 2022, but figures from 2021 were used to calculate my payment plan.

What's interesting is that with the start of the war in Ukraine in February 2022, prices of food and electricity increased drastically. For example, the cost of food and drinks was at an all-time high in February 2023, having increased 16.3% from the previous year. Also in 2022, electricity prices rose by 40 percent.

To recap, I had an allowance of €930 to cover all basic living costs for a month. With the increase in the price of food and electricity, we could not keep up. Especially considering we lived in a 2-story house with direct electric heating. The electricity bills alone were through the roof. In 2023, Finland passed a law (276/2023) that gave people financial relief in the form of being able to receive an up to 120-day extended payment time for their electricity bill. But of course, there is always a catch. As in the case for us, for bills that were past their due date, this extension was not applicable. On another note, this relief came way too late, again showing how policy lags behind the world we live in.

Can you imagine what this did, living under such extreme financial restraints?

Some might say, well, this is every day for me. To those, I am deeply sorry and sympathize, as no one should have to live by the poverty line.

That is why education and a stable job are so important. But in these turbulent times, with the economy as it is, even that stable job is not a given.

It's been stressful times for many, but what a person goes through emotionally whilst in the debt adjustment, it's something completely else.

DEBT ADJUSTMENT AND ITS EMOTIONAL TOLL

To truly grasp the emotional toll of the debt adjustment process we need to understand the nature of stress itself. The foundational definition comes from Hans Selye (1907-1982) a Canadian-Hungarian endocrinologist widely considered as the founder of stress theory. He defined stress as:

",an acute threat to the homeostasis of an organism. It may be real (physical), or perceived (psychological) and posed by events in the outside world or from within..."

The disruption to our bodies natural balance, or homeostasis is the scientific basis for the profound emotional and physical suffering that follows. Lets start with the emotional toll.

In 2019 my homeostasis was shattered by a series of what are known as Stressful Life Events, or SLEs.

A divorce, a move, death of my beloved pet, and the impending job loss from my company's bankruptcy all happened at once. These are textbook examples of acute stressors; short-lived events that trigger the body's fligh-or-flight response. In a normal acute stress reaction, the body releases hormones like adrenaline and cortisol, leading to a temporary increase in heart rate and blood pressure. Crucially these levels are meant to return to a normal once the threat has passed.

But for me the threat never passed. Instead my companies bankruptcy what in other countries would've been the end to a crisis, for me was the beginning of a multi-year ordeal; the debt adjustment program. This is where acute stress turned into chronic stress. My body's alarm system was stuck in the "on" position for years. The result was an ongoing loop of shame, hopelessness, isolation, and constant anger. It took me years to understand these weren't just feelings, but the direct emotional symptoms of a body and mind subjected to relentless chronic stress due to the financial stress I was constantly under.

Mieli Ry, a top organization on Mental Health in Finland published a report in 2023, "The Effects of Over-Indebtedness on Daily Life and Mental Health in Families with Children ." The results were as can be expected. People who suffer from financial and debt problems are more at risk to suffer from mental health illnesses such as depression and anxiety. Insomnia is also general. In addition those who suffer from being in debt experience physical symptoms, and frequency of illness.

Furthermore a report by Aapo Hiilamo from Mieli Ry showed that specifically debt difficulties lead to worry, shame and anxiety over the consequences of payment penalties as well as financial and social problems.

In Finland, what happens when your company goes bankrupt and you are in the debt adjustment, you loose your credit record ( luottotiedot in Finnish). This means you can literally not do anything involving some type of contract. You want to move, good luck finding a place to live, everyone checks your credit rating, and while this is natural, Finns are vey hesitant to rent to someone who does not have one. No explanation, how solid works. There are some companies that rent to people without a credit record, but those apartment buildings bare a stark difference to what people might have been used to. Then you manage to rent a flat say, but you won't be able to get electricity, as electricity providers won't give you a contract. Same goes pretty much everything. In comparison in the United States, even with bad credit, you can still get utilities, you just have to pay a deposit, or get a letter of guarantee. In general in the U.S. there are mediaries that can help someone with a poor rating, when in Finland you are stuck unless someone takes out something in your name.

The situation above is something I experienced when I was looking for a new place to live, and found it nearly impossible to find a flat, and had to settle on my current location. And you can bet I was so ashamed, and the amount of anxiety is caused. It took me a long time to come to terms with my current reality. Thank god I'm at peace with my living situation now, but for a long time it depressed me.

Indirectly indebtedness creates other types of problems. It may also make it harder to get employed since an employer might require a clean credit rating. I was flabbergasted when at a recent job interview I was asked about my debt adjustment, and more so even when I mentioned the fact that it had ended the previous month, it seemed to me my answer was not adequate. A friend had told me for a long time that me being so transparent about my bankruptcy might be key to me not getting employed as I have been on the lookout for a new job since my current one was ending soon.

THIS is exactly what needs to be changed. It seems ludicrous that in this day and age people are persecuted against for their financial situation. It makes me angry when I look at Finland's economy and the dire state it has been in for YEARS. All I wanted to do was create a business, employ people; which I did- two. And of course to grow my business. So while this did not happen, what did happen was I am punished and shamed, and made to feel like the scum of the earth.

Finland's economy never recovered from the global financial crisis. During the good ole days of Nokia, between 2000 and 2008 Finland's productivity grew by a total of 14.6%, but since the global financial crisis labour productivity has only grown a total of 1.1% from 2009-2023. Also since the crisis Finland's GDP per capita has not grown.

The Bank of Finland itself is calling for new investment, new skills and new growth. My ultimate goal was to contribute to that. Yet when my business failed, Finland's insolvency legislation, specifically the Debt Adjustment Act didn't see an entrepreneur who needs support to try again. Instead it treats people in a way that punishes risk-taking, and discourages the very entrepreneurial activity this country needs the most. This has been my mantra for years now, in order for Finland's economy to gow, entrepreneurship should be supported and nurtured, not frowned upon. The debt adjustment robs a person of their dignity, and puts their life on hold for 3-5 years, all while they could be contributing to the economy.

For example, second time founders, when given the opportunity have an average success rate of 30 percent. Compare that to first-time founders who have an 18% rate of success. This takes me to a topic dear to my heart, the culture of failure which is prevalent in Finnish society. Not only does it discourage entrepreneurship, but when someone fails, they will FEEL IT from everywhere.

To recap, the emotional toll of the debt adjustment is rough. But so is the toll it takes on your body.

PHYSICAL TOLL OF DEBT ADJUSTMENT

We all know that stress can wreak havoc on the body. A simple example most have felt as some point is the anxiety before a big presentation. That nervous, sinkking feeling- the 'pit in your stomach,'- is a direct, physical manifestation of acute stress.

In cases of chronic stress, take the example of panic attacks I started having sometime in 2020. I had never experienced one before, but they became a constant in my life. The feeling of my heart racing, shortness of breath, being unable to calm down. Long-term stress often leads to issues like anxiety, insomnia, and high blood pressure, which in turn increase the risk of developing chronic diseases such as heart disease, diabetes, depression, and obesity.

Furthermore stress leads to a disturbance of the brain-gutmicrobiota axis, otherwise known as the BGA. This results in the development of different gastrointestinal diseases. Coincidence I was diagnosed with diverticulitis in 2021? Non-stop insomnia over the course of many years, something else I never had a problem with.

The biggie for me was what it did to my immune system, could it be a compromised gut barrier, a condition known as 'leaky gut?'

Research provides a clear answer. One of the most damaging effects of chronic stress is an "increase in intestinal permeability." This means the protective lining of the intestines weakens, allowing bacteria to "leak" into the bloodstream.

This process attacked my body on two distinct fronts. The first was an internal battle, where the inflammation was a direct result of my own gut bacteria leaking into my system. The second front was at the border; my immune system, exhausted by the internal fight, was left defenseless against everyday viruses and bacteria I encountered.

This is what it means in real life: my body was fighting a war on two fronts. My body was spending all its energy fighting on the inside, leaving it defenseless against everyting else.

For me this translated into a constant state of sickness for nearly three years. Was it any wonder I was in a perpetual "flu state," catching every virus that went around? At the time it was frustrating because many close to me didn't understand it, even questioning me being sick, as if I was pretending to feel unwell.

In the end, my body became the evidence. Every panic attack, every sleepless night, and every bout of illness was a testament to the damage being done The emotional toll can be dismissed, but the physical is an undeniable record of the harm inflicted by a system that breaks people down instead of helping them rebuild.

CALL FOR REFORM

What's the worst than can happen in this situation, ask yourself.

A 2025 Norwegian study by Carla Hughes and Åsmund Hermansen for the Scandinavian Journal of Public Health titled, "Payment Problems and Suicide: Life Under Financial Strain," the authors studied the impact of payment problems on suicide. From their longitudinal study they found that those facing payment problems within the Norwegian population between 2009 and 2018 were at higher risk of suicide, this is both men and women. Furthermore when adjusting for demographic variables, they found that women who were experiencing financial hardship to be ever more susceptible to suicide in comparison to their male counterparts. The study suggests more protection is required for those coping with financial issues and highlights an important area for improvement within gender-sensitive health and social interventions.

Same can be applied to Finland. Many international studies have shown that financial woes can in addition to depression and anxiety disorders lead to self-harm. Furthermore those at high risk for suicide are people with mental health disorders and those who have previously attempted suicide. Those discharged from a psychiatric hospital have an extremely high risk of suicide. There is also a connection between those who have suffered traumatic and stressful events to suicide.

Annually more than 700,000 people die by suicide and the World Health Organisation has characterised suicide as a serious 'universal public health issue.' And so it should be. In Finland 752 people committed suicide in 2023.

If I go back, to some of my darker moments when I felt like there was no light at the end of the tunnel. Might things be easier for all if I just gave up? The inability to share these thoughts with anyone. Bedridden with a severe spell of depression that keeps you in bed weeks on end. At times I literally felt I was drowning, and couldn´t catch my breath.

No one should be made to feel this way. Entrepreneurship itself HARD AS Ht Debt ELL. Then bankruptcy in Finland. Following a long process of applying to and getting into the Debt Adjustment. Only to make your life unliveable.

Policy makers need a wake up call to the reality of real life in Finland.

It's easy for them to apply these figures when the system they use is flawed. It's as if they are creating a budget for a struggling family using grocery prices that are just don't align with the real cost of food, assuming tthat everyone in the family is healthy, all while drafting this plan from the comfort of their penthouse office. The numbers might add up on their excel, but they crumble upon contact with the harsh reality of inflation an the complex needs of real households.

They don't disappear when someone enters the debt adjustment. It's like what are you going to do, blame children for one of their parents trying to give them a better life by starting their own business? They failed, so let's make sure the whole family suffers. It isn't as if children cant sense when a parent is stressed. Why shoul td children be put to suffer? Would they be better off it the toll was too much for that parent and they took their own life?

Surely there are better options. Surely Finland can do better, especially considering the financial situation they are in. It would be in their best interest to increase number of businesses operating in Finland, but with the way they treat those who have gone through a bankruptcy they are missing on a massive out on a massive source of economic growth and potential.

What am I, and thousands of others like me in this equation? We are the very human capital the Bank of Finland says the country desperately needs to secure its future. By punishing failure instead of fostering a second change, the current Debt Adjustment Act is actively destroying the exact resource it should be trying to rebuild.